Probably you know the fantastic 1983 hit single by German band Nena called 99 Luftballons

If you read the lyrics of the song, you will see that 99 ballons are metaphors for peace.

Imagine that, inspired by this, you decide that you would like to establish a trust to launch 99 ballons into the sky every Tuesday as a symbol of peace.

Can you?

Czech Trusts are great for Czech people.

On the other hand, they are not normally considered as ‘export’ products. That’s because for people who live outside the Czech Republic there are other jurisdictions that offer more attractive alternatives.

But there is one, not very well known, exception to that rule. It’s an area in which Czech Trusts excel, and in which they are able to deliver outcomes that other countries cannot match. That’s the area of non-charitable purpose trusts

Before we explain what a non-purpose charitable trust is, we need to explain what a purpose trust is. To do that, we need to take a brief look at some important legal theory. We usually try to avoid talking about legal theory in these articles, basically because it is mostly quite boring. But in this case, I think the theory is interesting and it is helpful because it helps us understand the special problem that Czech Trusts can solve.

The piece of theory in question is the Three Certainties.

According to the law in most countries, the three certainties are the three essential things that you need if you want to create a valid trust. If you create something which does not have all three of these things, then you may have created a legally valid thing, but it probably isn’t a trust.

The first certainty is the certainty of intention.

The second certainty, certainty of subject matter.

The third certainty is the certainty of objects

The first certainly, the certainty of intention, means that it must be clear that the person who created the trust actually intended to do that (and not intend to do something else). Sometimes this a question of mistake or misunderstanding, but more often this issue comes up in the area of asset protection. Was the founder’s goal to really take care of his family? Or perhaps their real intention was to defraud their creditors, rather than to create a real trust for the benefit of future generations?

The second certainty, the certainty of subject matter, means that we need to know what is actually in the trust. If you put a house in your trust, then that is clear enough. However, if you say “All my good stuff”, it’s not clear to the trustees what’s good and what’s not good. If the trustees do not clearly know what is in the trust (and what is not), then it’s not valid.

But it is the third certainty, the certainty of objects, that is the most interesting one for today’s article.

This certainty means that we have to know who the trust exists for. For most trusts, that’s easy to answer. The trust is for the people who will get the benefit, in other words, the beneficiaries. So for a trust to be valid we need to know who the beneficiaries are, or at least have some clear system for working out who they are.

So, to recap, a trust needs intention, it needs some things to be in the trust, and it needs some people who will get the benefit.

And that’s where the idea of a trust for a purpose starts to get interesting.

What is a Purpose?

A purpose is limited only by your imagination.

The Royal Society for the Prevention of Cruelty to Animals (the RSPCA) was founded in 1824 and is the oldest and largest animal welfare charity in the world. According to its website its purpose is:

to inspire everyone to create a better world for every animal.

That’s a fantastic purpose. Here is another purpose:

to hold an annual hockey competition to find the champion team in the Dominion of Canada

Perhaps you know the Stanley Cup? It was established in 1892 as a trust and that was its original purpose

Here are some more purposes:

To award an annual prize to the best female economist in France

To maintain the village tennis court

To encourage the playing of tiddlywinks in Mexico

To support the election of Jára Cimrman as President

To look after my cat Tiddles after I die

To send the President a new pair of socks every Friday

To inflate and release 99 ballons every Tuesday

There really is no limit on what a purpose can be. Some purposes are positive and useful, others are not. Some purposes can be silly. Some of them have a great public benefit, but other purposes can be ‘private’

But we have a problem. Remember the three certainties? Certainty 3 says that a trust must be for someone. A purpose is not someone. (Even though he is lovely, Mr Tiddles is a cat, and he’s also not a person either).

So can you make a trust like this – which benefits a purpose rather than a person?

International Problems

The short answer in many countries is: no, you cannot. Judges in these countries do not like purpose trusts.

There was a quite famous case from 1882 called Brown v. Burdett. In that case the purpose was that a lady wanted her house to be boarded up with “good long nails to be bent down on the inside”, but for some reason with her clock remaining inside, for twenty years.

Unlike some of the purposes above, this one is perhaps not quite so positive and constructive. The judge in that case decided that the trust was not valid – because it was ‘useless’

There are two other reasons that courts don’t like purpose trusts. First, in the case of a normal trust with beneficiaries, we have somebody (the beneficiaries) who can keep an eye on the trustees and make sure that they are doing a good job. With a purpose trust, that person is missing

But more fundamentally, WHO is it actually for? In the opinion of the courts, you can’t just take money and put it in a bucket forever, with no person at the end of the line. And that is the reason that in most of the world, trusts need, in the end. to be for people.

Trusts without people do not satisfy that third certainty – and so, even though they might be fantastically useful – they are not valid.

Exception and Solutions

As you may have noticed, the RSPCA does actually exist. It’s an example of the first exception: charities. In many countries, charities are established as trusts, because a trust is a fantastic structure for running something like a charity, and charities generally, by definition, are established for purposes.

In the UK, for example, there is a list of purposes set out in law, and if your charitable purpose trust complies, then you can establish your trust. However, this is very strictly regulated, controlled and supervised by the Charity’s Commissioner. That means that it’s expensive and complicated and beyond the reach of ordinary people. It also only works for charitable purposes.

But what if your purpose is not charitable?

There a couple of additional exceptions in many counties including looking after pets and maintaining graves.

But otherwise, you are out of luck, and I am sorry to inform you that your plan to launch 99 ballons every Tuesday will not come to fruition.

Czech to the Rescue

But that’s where the Czech Republic comes to the rescue.

Your balloon plan won’t work in most countries, but it will work in the Czech Republic

That’s because section Section 1448 of the Civil Code says:

A trust fund is created by setting aside assets from the founder’s ownership in such a way that the founder entrusts the asset to the administrator for a specific purpose

There is no rule in Czech law that says there needs to be a beneficiary and the three certainties do not apply in Czech, so there is nothing to stop you from realising your plan.

Not only that, but we think such a trust could actually be quite tax efficient. It would not make any profit and, because there is nobody who gets the money, there is presumably also nobody who would need to pay tax.1

So this is something that is handy, not just for Czech people, but for everyone else in the world who cares about ballons and world peace.

There is no reason either why the ballons need to be released in Czech either. You might live in Albania and you might want to release the balloons there. There is nothing we can think of to stop you setting up a Czech Trust to do this.

So this could even be the Czech Republic’s next great export program!

__________________________________________________________________________

1 We are not tax advisers so if you do set up a balloon trust you should seek specialist advice on this point.

Many ordinary Czech people already know something about trusts, and they are increasingly interested in knowing more. They are interested not just in how trusts can help the wealthy, but also how they can help their own families. We suppose this is the main reason behind the success of our book. Before our book came out there was no easily accessible source of this information.

Many ordinary Czech people already know something about trusts, and they are increasingly interested in knowing more. They are interested not just in how trusts can help the wealthy, but also how they can help their own families. We suppose this is the main reason behind the success of our book. Before our book came out there was no easily accessible source of this information.

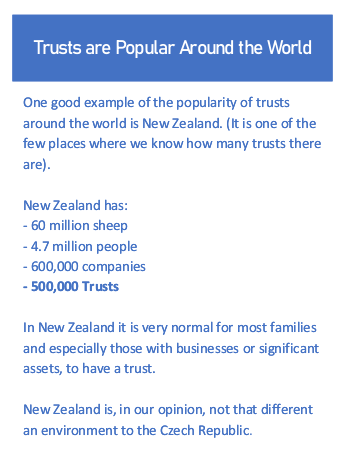

Philip lives in New Zealand As we have mentioned in the past, and as the box to the right illustrates, unlike the Czech Republic, New Zealand is a country of trusts.

Philip lives in New Zealand As we have mentioned in the past, and as the box to the right illustrates, unlike the Czech Republic, New Zealand is a country of trusts.